- SEC secures $1.1M after crypto fraud defendant skips court.

- Stemy Coin falsely claimed backing from labs and stem cells.

- Judge issues permanent ban and heavy penalties for violations.

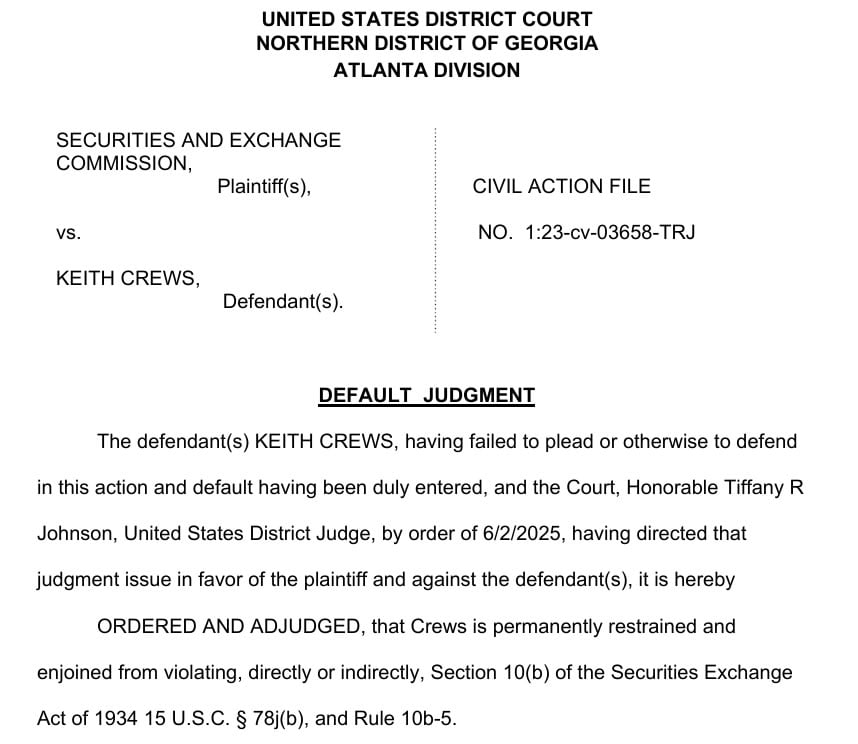

The U.S. Securities and Exchange Commission secured a $1.1 million judgment after the defendant failed to appear in court. On June 3, a federal judge in Georgia issued a default ruling against Keith Crews, who had ignored an SEC complaint filed in August 2023.

The court found that Crews violated federal securities laws through fraudulent activities tied to a digital token known as “Stemy Coin.” The 69-year-old, based in Kennesaw, operated through two entities, Stem Biotech LLC and Four Square Biz LLC. The SEC alleged that between October 2019 and May 2021, Crews misled nearly 200 individuals and secured over $800,000.

Disgorgement, Civil Penalties, and a Permanent Ban

U.S. District Judge Tiffany Johnson ordered over $1.1 million in total penalties. The ruling included $530,000 in illicit profits, nearly $51,000 in interest, and a $530,000 civil fine. The judgment also imposes a permanent injunction, barring Crews from violating securities laws going forward.

The SEC said Crews lured investors by making false claims about advanced medical products and gold-backed crypto. He claimed his firm had working labs and biotech partnerships, but no such infrastructure or affiliations existed. Many participants were approached through church groups and community ties.

The agency made it clear in the complaint that Crews chose targeted those unable to defend their assets. The participants were made to think the research concerned revolutionary work with stem cells. Actually, the company did not produce anything, rent no space and partnered with nobody.

Misrepresentations and Unregistered Securities Offerings

Crews allegedly promoted unregistered securities while presenting Stemy Coin as backed by tangible assets and medical science. His companies falsely advertised affiliations with healthcare professionals and research institutions. The SEC said those statements had no basis in fact.

The regulator brought charges under fraud and registration provisions of the Securities and Exchange Acts. Crews did not respond to any legal summons or defend against the allegations. This led the court to grant a default ruling in the SEC’s favor.

This decision is made as the SEC appears to have put crypto enforcement on a pause. It remains uncommon for the agency to get legal approval in cases about digital assets.

This case emphasizes the continuous issues surrounding unregistered offerings and false statements in raising money for cryptocurrencies.